Substack Should Enable Check Payments and Save Literally a Few Million Dollars

I am too Autistic Not to Write This

Update: See the bottom of the post for better numbers, facts, and additional autism.

So, it’s been a lot lately.

You’ve probably read my last couple posts and thought, “Oh yeah, strange assortment of things here. Political essays, stuff about AI, personal stories… maybe that’s warranted because there’s been some personal loss there recently. Unusual guy but aren’t we all, really?” Still, with such a wide assortment of posts, what is this substack really about?

I think it’s mostly about how sometimes I wake up too early in the morning and have strong opinions about things. Seriously, woke up at 1:30am this morning and can’t get back to bed.

FYI: As soon as I realized the panic attacks were back I made an appointment to see a therapist, a nutritionist, and a doctor so I could get something to help me actually do my job. I got a prescription for some beta blockers that I have used exactly one time so far and they worked really well. I’m no longer concerned about not being able to function which ironically means I don’t seem to need the medication now. I’m also supposed to eat lavender so we’ll see how that goes.

Now, onto the next logical topic. Transaction management.

In real life I do banking stuff. You may have noticed this substack is not paid but even though that’s the case I know a lot about how that all happens on the back end, or at least I know how it works internally at a bank. There are multiple different strange ways you can process payments that almost nobody uses like Western Union but for this essay let’s focus on just two that are more common: Check and Card.

Whenever you swipe your Card did you know that the transaction isn’t actually free? There are hidden costs paid by the merchant. So if you buy an $10.00 banana some portion of that money is being paid to either VISA or Mastercard and that applies both to your debit and credit card. I’m guessing it would be something like $0.60 for the fee in this case. However, when you pay that fee you had the added benefit of receiving the money right away. That’s how VISA and Mastercard make their money.

When you pay with a check you feel like you’re in the Stone Age. Write on a little piece of paper? Come on, what a joke. On the back-end it’s still all electronic and you don’t actually need a physical check to process a check payment. You’ll also notice that certain business only allow you to pay with checks. It’s because of the VISA and Mastercard fees being much higher to process and cutting into the profits of those companies. Credit Cards especially don’t want you to pay with a debit card because they make money on the transaction costs and interest they charge you as well, so if you were to buy everything with your credit card and then pay it off with a debit card you could actually make your account cost money to maintain instead of earn money. Inside of a bank, the cost to transact what is called an ACH (Automated Clearing House) check draft is a fraction of one penny. Might as well be free. Outside of the bank it’s about 0.8% of the total transaction because you have to pay a payment processor to act as the middleman. So that ten dollar banana you bought with the debit card that had a $0.60 transaction fee only costs about $0.08 to transact with a check. However, you also have to wait one to five days to receive the money and it can take even longer than that to clear.

Why does this matter to Substack?

There are certain use-cases where you are happy to pay a card processing fee. You are worried the customer doesn’t actually have the money, there is a high chance they’re trying to screw you over, and you pay the fee to have the money cleared right away. Easy choice.

Substack isn’t like that. Substack is an ongoing monthly expense. They have history with their customers. What are the odds you’ll have $5.00 one month and you won’t have it the next month? Or that you are subscribing only to turn it around with a “Gotcha!” and rip off Jesse Singal or whoever? Very low. Also, if the money is there and promised why would you need it to come in immediately if you stagger the dates you’re receiving money? You can keep your cash flow very liquid, meaning you don’t put yourself in a spot where you have to wait once a month to get paid. Some amount of money will just be flowing in to your coffers all the time. The other nice thing about checking account numbers is that they don’t expire. People tend to get a new credit card or debit card number every few years and then their subscriptions just stop working.

Let’s build the business case and we’ll talk about two things. The cost savings of ACH vs Card transactions and then the cost savings of batch transactions.

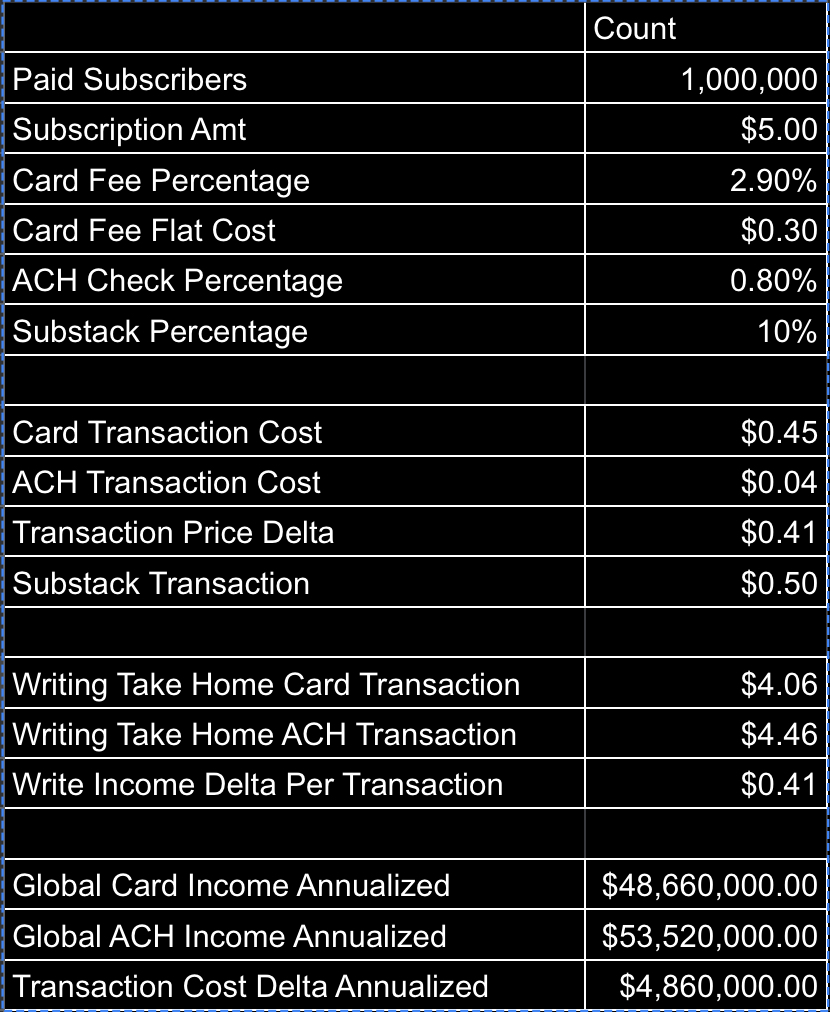

For the sake of making this easy let’s say substack has a million paying subscribers and they all pay $5/month. The numbers are no doubt different than that and I could spend several hours building a spreadsheet to get the exact figure. For us, this is easy enough.

Note: I got some numbers wrong here and some of this was easy to answer if you see the below.

Substack uses a company called Square to transact its card payments. I looked and tried to switch over a subscription to a checking account and could not. Here’s what looks like just so you know. The only option is card.

Square charges 2.95% of the transaction cost plus a $0.30 flat fee. So your $5.00 subscription by the time it leaves you and goes to Substack is actually $4.69 because it cost $0.31 to move the payment. Substack takes a 10% cut but I don’t know if they do that off the $5.00 or the $4.69 but to make the math easy we’ll do it off the $5.00 and say it’s $0.50. That has now reduced your $5.00 monthly subscription to $4.19. But wait! Substack has received the money but they need to send it on to you! This is where my knowledge gets a bit fuzzy. Either Square is agreeing to split the money like that and do all of this in a single transaction or else Substack has to hit square a second time and move the money again. Or they are doing something sensible like using a whole different transaction processor to move the money out as an ACH Direct Deposit. If Square is involved in this transaction twice you are going to be out another $0.31 and either Substack is taking that haircut or you are at the subscription side.

Let’s talk about how much that costs over a year and how much money Substack pays for just these transaction costs. That $0.31 in the course of a year costs $3.72 per customer. Let’s say Substack isn’t having to pay anything extra to move the money around between themselves and the writer. At a minimum, if Substack has a million paying subscribers, they are paying $3.72 million dollars per year in card transaction costs. At most if they are having to move the money around again using Square, it’s $7.44 million.

There’s other stuff that could throw those numbers off like Square cutting a deal to give them lower per transaction costs and I would expect there’s something like that going on as most companies like that have some volume tier discount model but it’s going to be in the right general neighborhood. Still, that’s between $3.72 million and $7.44 million just for moving money around that doesn’t really touch your core product. Nobody cares how their payment transacts. They just want to support stuff they like.

Now let’s talk about check drafts. We’re all older in my experience. We have checkbooks. Probably don’t use them a lot but go pull out that thing. Find the routing number, the first nine digits in the bottom left. You can enter all of that online the same way you do with a debit card. This is ancient technology but it’s cheap. I looked up the per transaction costs for a company called Stripe which is how I came up with the 0.8% figure. Let’s do that same $5.00 transaction. How much do you pay this time? $0.04. 4 cents. Four pennies. That’s it! If you have to move the money again that’s maybe $0.08. 8 cents. Eight pennies. So your multimillion dollar transaction cost just went down to $40,000 or $80,000. Yeah you have to wait for the money but so what? You’re getting a constant roll-over.

That’s small enough that it’s hardly worth subtracting from the card transaction fees. You’re probably saving a couple million dollars every year going forward even if Square is giving you lower costs for high volume. In real life, not everybody makes the switch and it tends to be inconvenient but if you press people on it and share the savings with the writers then you can get real incentive to switch.

Let’s say Scott Alexander has 10,000 paying subscribers at $5/mos. Those aren’t the real figures. I’m just giving an example. Let’s say he’s getting $4.19 of each of those subscriptions because they’re from cards so he is bringing home $41,900 each month. Now let’s say we switch this around. Do all those as check transactions. Harder to do upfront maybe but here is where you’d feel the savings. That’s $4.19 was for cards. But remember we are now only paying $0.08 maximum to move the money with a check. So now let’s say Scott can take home the whole thing minus the check fees and substack’s cut. So we’ve got $5.00-$0.08-$0.50= $4.42.

Now instead of taking home $41,900 each month Scott takes home $44,200 an increase of $2,300 or over the course of a year $27,600. A new car of money, even if it’s a KIA, because we moved the same amount of money more cheaply. Again, I’m putting Substack at the maximum disadvantage in the check scenario and the greatest advantage in the card scenario so in real life these savings might be even bigger.

Okay, okay, let’s say you can’t do this for some reason. Maybe Square would flip out if you used Stripe as well. Your discounts are contingent on you only doing cards, yada yada yada There’s still a way for Substack to save money and pass it on to writers and still use card payments.

Batch processing.

I am subscribed to multiple substacks. Shoutout to PirateWires, Blocked and Reported, Scott Alexander, and Singal-Minded. Let’s say that between all of those I am paying $20.00/month. I don’t remember off the top of my head that I actually pay but let’s say it’s that for the sake of math.

On my credit card statement each month these all show up as separate transactions. I don’t just pay Substack once, I pay Substack four different times. So take that $0.31 Square Transaction fee and multiple it by four to $1.24 each month and annualize it to $14.88. Again, I’m assuming Substack is only paying the Square Transaction fee one time and getting the money split between them and the writer in one go. I don’t know how that works. It might be as high as $30.00 for this to all happen each year out of the total $240 I am paying for my subscriptions. I hope not.

Let’s say that out of Substack’s million hypothetical paying subscribers that 100,000 of us are subscribed to four Substacks and paying $20/month. So the total cost for all of us each year to do all four of our transactions separately is $1,488,000 out of the $24,000,000 that Substack is moving around every year for this tier of customer.

Let’s now say that Substack does all of this in one single transaction and Square is able to divvy up the money correctly. I’m less sure that Square can do this but I don’t have my eyes under the hood. It could also be the case that they could receive the money as a card transaction but then deposit it as a check transaction to the writer which would mitigate a lot of complexities of this and I hope they are doing this. By taking the money all at once instead of paying that flat fee of $0.30 for each of the four separate transactions Substack is only paying it one time plus 2.95% of the $20 which is $0.59. So the total monthly cost to transact my four substack payments is $0.89 as opposed to the $1.24 above. Annualize both those figures and processing all the payments at once costs you $10.68 versus the $14.88 or just $1,068,000 for the whole customer populations, a savings of $420,000 each year!

Substack is likely already aware of some of this because they push you to do a yearly subscription. Part of that is customer preference and part is because the less times you have to touch the money the cheaper it is to transact. But look at that example above an annual subscription costs $50 and a monthly subscription costs $5/month or $60/year. You’ve giving up $10/year and even though it doesn’t cost the $3.72 a year it costs to move the money for a monthly subscription it still costs you $2.07! Ouch! Very ouch!

Changing a few simple things with billing ends up savings a few million dollars every year! And what’s more it scales with the business so if you have twice as much revenue you save twice as much money. Yes, you would have one time costs for the changes plus some maintenance, plus some cost splitting with the writers to incentivize the change, but I want to say the Substack team is something like 90 people. This could be enough extra money to pay for ten additional staff members. Split the savings with the writers, encourage readers to use one method over the other and you have permanent ongoing savings.

Of course in real life you don’t get 100% conversion and you don’t want to turn away people with cards but again, these small things matter over long periods of time. The Free Press has 50,000 paying subscribers. Their minimum charge is $8/month. They pay $0.54 of that each month in transaction costs for their cards versus again $0.06 a price different of $0.48 cents. Multiply that by 50,000 and you get $24,000 each month just disappearing. Over the course of a year that’s $288,000. Not going to Substack or the Free Press but just to move the money around for the people who want to pay for those things.

You are all welcome and I’m going to go sit in front of my SAD lamp now.

Update:

Okay, I made some embarrassing mistakes here that were easy to resolve. The first is that 2.95% of $5 is closer to $0.15 than $0.01 and I’m not sure how I did that other than that my sleep has been garbage and when you work in banking you lose the ability to do basic multiplication without a spreadsheet. The second is that Substack uses Stripe as their payment processor not Square. Both of these mistakes push the numbers in favor of ACH transactions.

The transaction cost is the same for card payments at both Stripe and Square, however this also means that there’s a native check payment processing ability with the Stripe payment processor Substack already uses. Also just by poking around I was able to determine that Substack does indeed push payments to writers via an ACH deposit meaning they are only paying the card transaction costs once per subscription per month.

One other quick point of clarification: an ACH Check Draft is not a paper check. It’s exactly like entering card information except you take the numbers from your check. There’s some legal stuff involved as far as the disclosures you see versus the card payment but otherwise it’s exactly the same. So the future with the cheaper transaction costs versus the higher transaction costs is basically just a few different entry forms on the “buy” page.

My guess is that this is roughly close to the actual numbers for the transaction costs. So if our assumptions hold true, and it’s trivial to update the spreadsheet to the actuals, there’s about $4.8 million per year that could be going to writers that is instead going to Stripe.

If Substack is built on long term subscribers they should move to default capturing of checking account information instead of card information. Your customers are people who are paying you every month for multiple months on end, not fly-by-nights who you only see a single time or very infrequently.

People won’t convert to paying customers as easily if you ask them to enter ACH info. This is completely irrational but very true. Higher conversion rate is likely worth more millions of dollars than using ACH would save.

I'm a little confused. Are you talking about literal paper checks? Or a direct transfer using the routing number and checking account number? The latter is what I experienced when I lived in Germany throughout the '90s. The Germans thought Americans were barbarians for not having their system, and I had to agree.

I can't imagine paper checks would be workable. It takes labor to process them - which can't be fully automated, or am I wrong? And you're going to have lots of people paying late, which would be a mess when we're talking about small-dollar amounts each month.

Wishing you a better night's sleep tonight!